As permitted by section 75B of the Income Tax Act, No. 58 of 1962, effective 1 January 2009, SARS has begun imposing a range of stringent penalties in respect of non-compliance by taxpayers, which includes:

- Failure to register as a taxpayer

- Failure to inform SARS of a change of address and other personal particulars

- Failure to submit Income Tax returns (ITR12) and other documents.

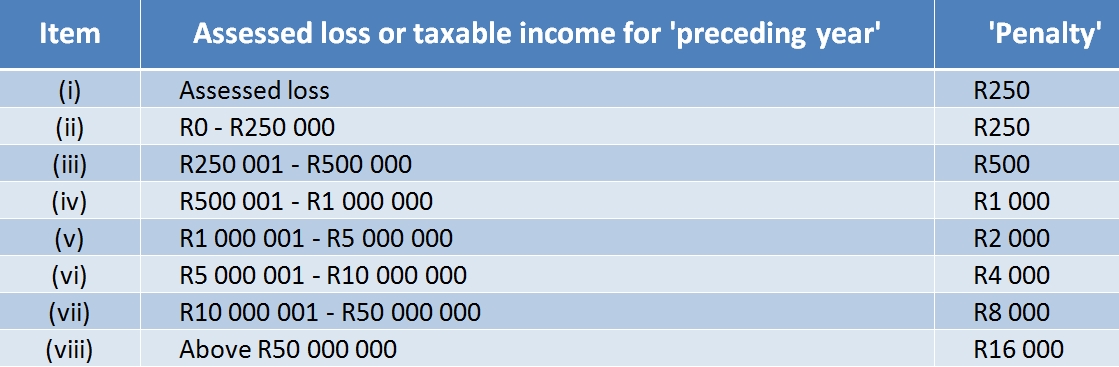

The abovementioned non-compliances are subject to a recurring penalty (this penalty will be charged each month until the non-compliance has been remedied). The amount of the penalty is determined according to the taxpayer's taxable income or assessed loss. The table below illustrates the penalty to be charged:

Contact us and we will help you with your admin penalties